Why an Option Shows Zero, Blank, or No Greeks: Missing Marks and Volatility

Last updated: July 1, 2026

An option — or a position holding options — that shows zero, a blank value, or no Greeks is almost always missing a required pricing input, not a worthless option. Unlike a future, which needs a single price, an option also needs a volatility input to be priced; if that's missing for the product and date, Molecule can't model-price it. This article explains that dependency, how to recognize it, what you can fix yourself, and how option value behaves around expiry.

Not covered here

Stale or missing price marks in general (copy-forward, curve source, the manual-mark override) → see the vendor stale-prices article and "Mark Levels."

A P&L or valuation number that looks wrong for non-option reasons (screen vs extract, resave to revalue, marks are per product) → see the P&L diagnosis article.

Option expiry, exercise, abandonment, and what exercise generates → see the option-expiry/exercise/P&S article. This article touches expiry only as it affects value .

Why options need more than a price

A linear product — a future, a swap, a physical forward — needs one thing to value: a price mark for the product and date. An option needs two:

the underlying price mark , and

a volatility input — an implied-volatility surface (or a flat vol) for that product and tenor. Implied vol is the market's expected price variability; a volatility surface isn't a single number but effectively a matrix indexed by strike (the option's exercise price) and tenor (the contract period).

An option is model-priced: Molecule runs an option-pricing model that takes the underlying price and the volatility input and returns a value plus the Greeks (the sensitivities — delta to the underlying price, gamma to delta, vega to volatility). If the volatility surface (or the underlying price) is missing for the relevant product and as-of date (the valuation date), the model can't run: the option shows zero or blank, and its Greeks are null.

There is no silent fallback. Molecule does not quietly substitute a simplified, intrinsic-only, or Black-Scholes-style estimate when the volatility input is missing — it shows no model value rather than a misleading one. So "my option is zero" or "my option has no delta" usually means a required pricing input is missing — most often the volatility surface (or the underlying price) for that product and date, though an option will also fail to price if the option product's pricing model isn't configured — not that the option is worthless.

Recognizing the cause

A few checks tell you which input is missing:

No Greeks plus a zero or blank value strongly points to a missing volatility surface for that product and as-of date. Greeks come out of the model; if the model couldn't run, there are no Greeks.

A linear product on the same underlying values fine, but the option doesn't. That isolates the volatility input specifically — the price mark is probably present; the vol input isn't. (A future needs only the price; the option needs the vol too.)

Check the specific date. The dependency is date-specific : confirm a vol (and price) mark exists for that product and that as-of date, not just "in general." See "Mark Levels" for reading which mark fed a valuation, and "Valuation & Relevant Products" for why no market data means no valuation.

If the price and the vol surface are both present for the date but the option still shows zero or blank, the option product's pricing model may not be set up. Every option product needs its option model (its model "flavor") configured before Molecule can price it; if that's missing, the option shows zero or blank with no Greeks even when the market data is fully loaded. This is a product-configuration item — an admin or support task, not a market-data upload.

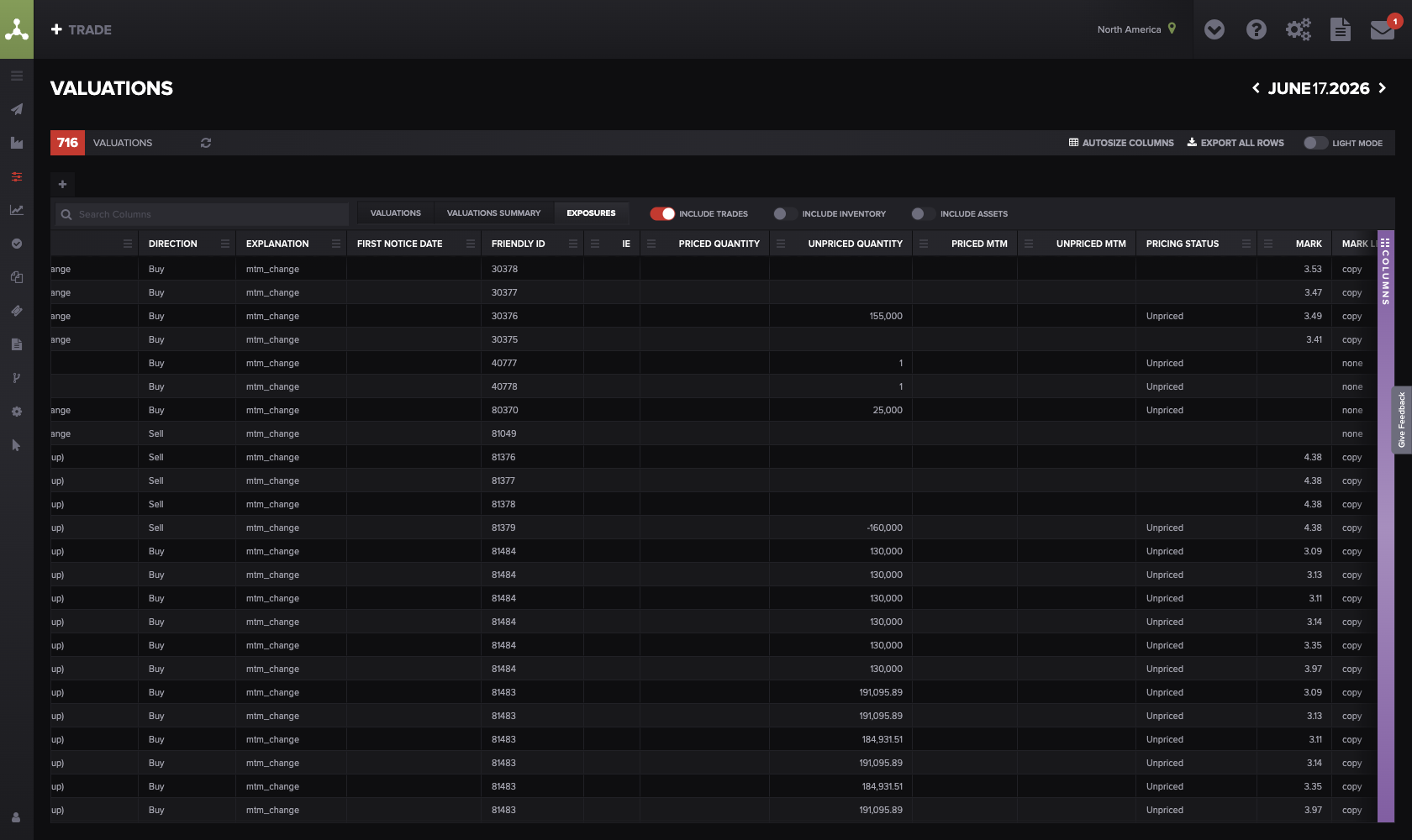

An option valuation

A blank option value with no Greeks usually means the volatility surface for that product and date isn't loaded — the model couldn't run. Alt text: A Molecule valuation row for an option showing a blank value and empty Greek columns.

Fixing it

If the underlying price mark is the gap, the general stale/missing-price remedies apply — including uploading a temporary mark. Rather than repeat the procedure here, see the vendor stale-prices article.

If the volatility surface is the gap, loading option volatilities is its own data task. Often this is something you can do yourself: when the gap is simply un-loaded vol data, an admin can upload the volatility surface (or a flat vol) for the product and date. When the gap is instead an upstream feed problem or a configuration issue, that's a support item. See the loading-option-volatilities article for the upload format and steps.

If marks and vols are present but the option still shows stale or zero after a change, a resave can force the trade to recompute: open it in edit mode and save (no changes needed).

⚠ One exception — don't resave a P&S-matched trade. Resaving a P&S-matched trade destroys the P&S match, with no automatic restoration. If the option position has been closed with P&S, see the option-expiry/exercise/P&S article before resaving.

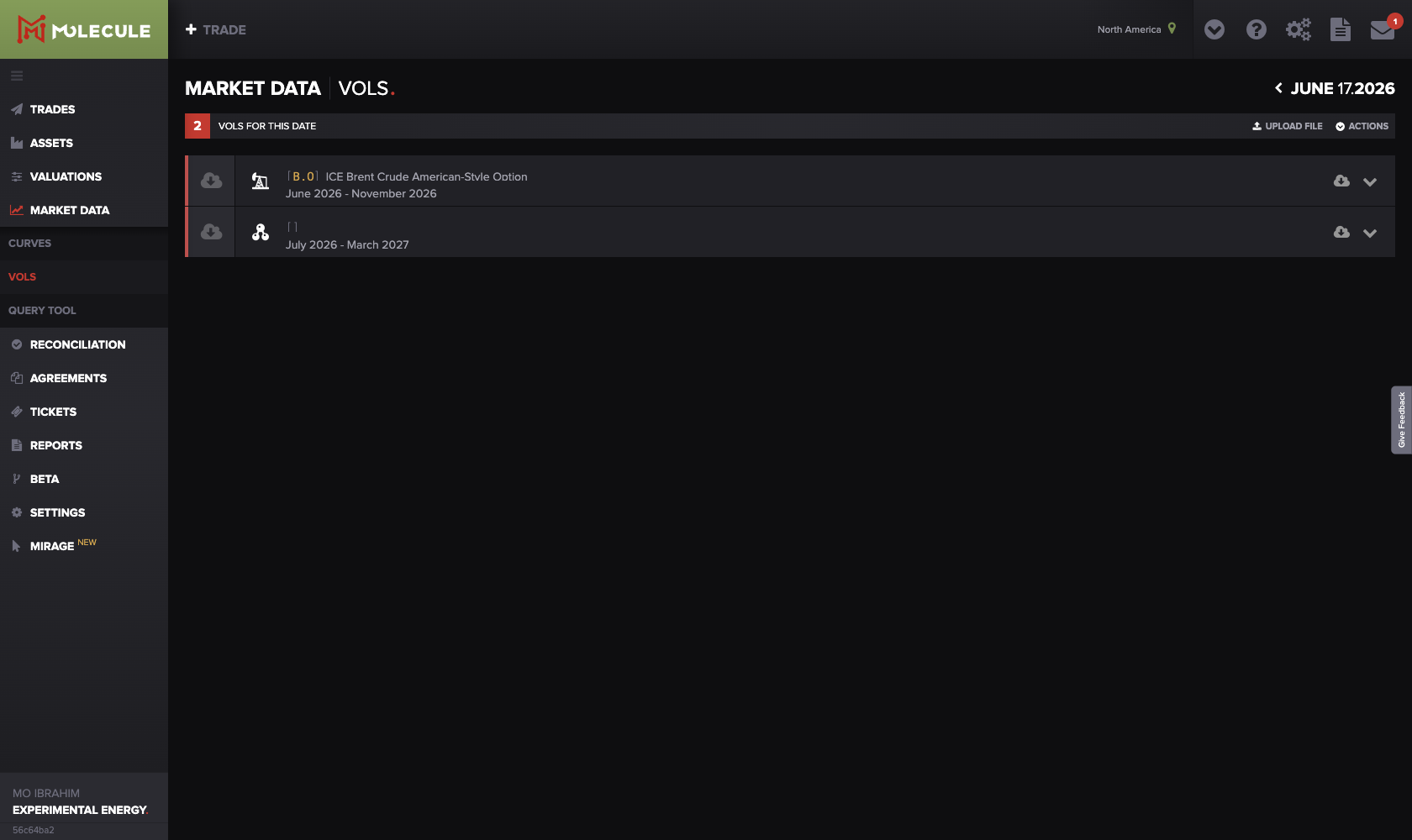

A volatility

The Market Data view for an option's volatility curve — one state where vol data exists for the as-of date and contract months, and one where it's absent — to show what "missing vols" looks like. Use a generic account.

Check Market Data for the option's volatility surface on the relevant date; a gap here is the usual cause of a blank option value. Alt text: The Molecule Market Data view comparing a present volatility surface with a missing one.

Option value around expiry

Option value behaves predictably as expiry nears — and what looks alarming is often expected:

Value converges to intrinsic. As time to expiry shrinks, the model value moves toward the option's intrinsic value (its in-the-money amount — what it's worth if exercised right now), because there's less time value left. Model value is the full model price (intrinsic plus time value); intrinsic value is just the in-the-money portion.

Greeks can spike near expiry. With very little time left, Greeks like gamma and vega can become very large. Unusual-looking Greeks right before expiry are usually mathematically expected, not a bug .

An exercised option settles at intrinsic value , not model value. What happens at expiry — automatic vs manual exercise, abandonment, and what an exercise generates — is the lifecycle topic; see the option-expiry/exercise/P&S article. Here we cover only the value behavior.

What to send support

If the self-checks don't resolve it, send support:

the option Trade ID(s) (Molecule's internal trade identifier) and the product,

the as-of date where it shows zero, blank, or no Greeks,

whether a linear product on the same underlying values correctly for that date (this helps isolate the volatility surface),

whether you expected a volatility surface to be loaded for that product and date, and

whether you've already tried loading the missing input, and via what path.

FAQ

My option shows zero — is it worthless?

Usually not. A zero or blank option value almost always means the volatility surface (or the underlying price) for that product and date isn't loaded, so the model couldn't price it— or the option product's pricing model isn't configured — not that the option has no value.

Why does my option have no delta or gamma?

Greeks come from the option-pricing model. If the volatility surface is missing, the model can't run, so there's no value and no Greeks. Load the missing vol (or price) for that date and the Greeks return.

The future values fine but the option doesn't — why?

A future needs only a price; an option also needs a volatility input. If the option is blank while a linear product on the same underlying values correctly, the volatility surface is the likely gap.

My option's Greeks look crazy right before expiry — is that a bug?

Usually not. As expiry approaches, value converges to intrinsic and Greeks like gamma and vega can spike. That behavior is mathematically expected.

How do I get the missing volatility loaded?

When the gap is just un-loaded vol data, an admin can often upload the volatility surface for the product and date — see the loading-option-volatilities article. If it's an upstream feed or configuration issue, contact support with the product, the volatility curve, and the date range.

Related articles

Editor: hyperlink each of these to its help.molecule.io article before publishing (URLs to be confirmed once web access is restored).

If you're still stuck after the checklist above, contact support@molecule.io with the details listed in "If none of these explain it."